Instrumental Variables

|

Software |

|

Overview

This page briefly describes instrumental variables and then provides an annotated resource list.

Description

Instrumental Variables (IV) estimation is used when the model has endogenous X’s. IV can thus be used to address the following important threats to internal validity:

1. Omitted variable bias from a variable that is correlated with X but is unobserved, so cannot be included in the regression

2. Errors-in-variables bias (X is measured with error)

3. Simultaneous causality bias (endogenous explanatory variables; X causes Y, Y causes X)

Instrumental variables regression can eliminate bias from these three sources

-

Sources of Bias – Omitted Variable, Measurement Error, Simultaneous Relationship

Omitted Variable

Consider the following regression modelwhich conforms with standard OLS assumptions. Suppose that the variable x2 is not observed. The estimated regression model is therefore

where ui=xi2+b2+vi. Regressors xk in x1 are therefore correlated with the error term u if they are correlated with the omitted variable x2. In case xi1 and xi2 are scalars, cov(xik, ui)=b2cov(xik,xi2).

-

Measurement Error

Consider the true regression modelwhich conforms the standard OLS assumptions. Suppose that the variable x*s only observed with an error

where the error v is uncorrelated with x* and with ui*. The estimated regression model uses x as a proxy for x*

where ui = ui*-b1vi. The regressor x is therefore correlated with the error term u as both depend on v. Assuming independence between v and

u*, the covariance in the above example is

-

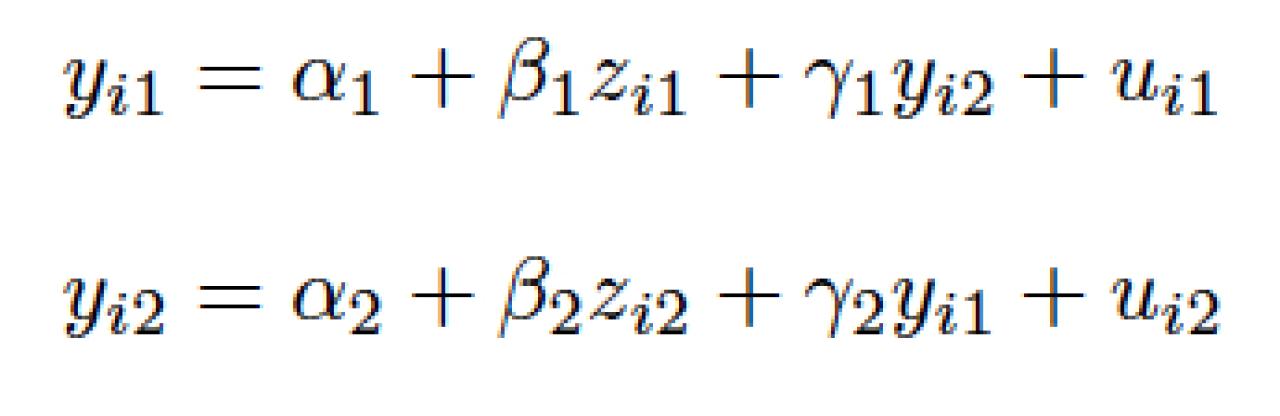

Simultaneous Relationship

Consider the following system of equationswhere we assume that both z1 and z2 are uncorrelated with both u1 and u2. This system is called a structural simultaneous equation system since y1 and y2 are simultenously determined. The regressor y2 depends on y1 through the second equation. As y1 is directly dependent on u1, the regressor y2 is also correlated with u1 and hence endogenous in the first equation. Assuming that u1 and u2 are uncorrelated, then

The above equation system is also described as reversed causality because the dependent variable y1 has a feedback effect on the regressor y2. In the above example z2 and z1 are straightforward instruments for IV estimation of the first and second equation, respectively.

Instrumental Variables: Intuition

-

An instrumental variable, Z is uncorrelated with the disturbance e but is correlated with X(e.g., proximity to college might be correlated with schooling but not with wage residuals)

-

With this new variable, the IV estimator should capture only the effects on Y of shifts in Xinduced by whereas the OLS estimator captures not only the direct effect of on but also the effect of the included measurement error and/or endogeneity

-

IV is not as efficient as OLS (especially if Z only weakly correlated with X, i.e. when we have so-called ‘weak instruments’) and only has large sample properties (consistency)

-

IV results in biased coefficients. The bias can be large in the case of weak instruments

Identification and Estimation

Compliance Status from Potential Outcome Framework

-

If we assume a situation where an experimenter implemented a randomized experiment where the participants are preschool children, in which the treatment is Watching Sesame Street TV Program, and the outcome of interest is score on letter recognition test

-

In this experiment, watching itself cannot be randoimzed but only encouragement to watch the show can be randomly assigned

-

Taking advantage of the randomization of encouragement, could esitmate a causal effect of watching for at least some of the people in the study

-

As shown above in the below, the children in the trial could be categorized according to their compliance status

|

Status |

Xi(1) |

Xi(0) |

|

Always Takers |

1 |

1 |

|

Never Takers |

0 |

0 |

|

Compliers |

1 |

0 |

|

Defilers |

0 |

1 |

-

Compliers are the only children for whom we will make inferences about the effect of watching Sesame Street and this effect is referred as the Complier Average Causal Effect (CACE)

Four Major Assumptions for IV

-

Ignorability of the instrument: The instrument should be randomized or conditionally randomized with respect to the outcome and treatment variables

-

Nonzero associaiton between IV and treatment variable: The instrument must have an effect on the treatment

-

Monotonicity: Assume that there were no children who would watch if they were not encouraged but who would not watch if they were encouraged (no defiers)

-

Exclusion restriction: The instrument has no direct effect on the outcome, except indirectly through the treatment

Wald Estimator and Two-Stage Least Squares Estimator: From the Sesame Street Example

|

Unit |

Xi(0) |

Xi(1) |

Status |

Z |

Yi(0) |

Yi(1) |

Yi(1)-Yi(0) |

|

1 |

0 |

1 |

Complier |

0 |

67 |

76 |

9 |

|

2 |

0 |

1 |

Complier |

0 |

72 |

80 |

8 |

|

3 |

0 |

0 |

Never Taker |

0 |

68 |

68 |

0 |

|

4 |

1 |

1 |

Always Taker |

0 |

76 |

76 |

0 |

|

5 |

1 |

1 |

Always Taker |

0 |

74 |

74 |

0 |

|

6 |

0 |

1 |

Complier |

1 |

67 |

76 |

9 |

|

7 |

0 |

1 |

Complier |

1 |

72 |

80 |

8 |

|

8 |

0 |

0 |

Never Taker |

1 |

68 |

68 |

0 |

|

9 |

1 |

1 |

Always Taker |

1 |

76 |

76 |

0 |

|

10 |

1 |

1 |

Always Taker |

1 |

74 |

74 |

0 |

. The Intent-to-treat effect (ITT) in the hypothetical table above for the 10 observations is an average of the effects for the 4 induced watchers, along with 6 zeros corresponding to the encouragement effects for the always takers and never takers:

ITT = (9+8+0+0+0+9+8+0+0+0)/10 = 8.5*(4/10) + 0*(6/10) = 3.4

. The effect of watching Sesame Street for the complier is 8.5 points and this is algebraically the same as the intent-to-treat effect (3.4) divided by the proportion of compliers (4/10). This ratio is called the Wald estimate

. But two-stage least squares is a more general estimation strategy with a regression framework, which allows for controlling covariates. And the required steps are follows:

– Regress the treatment variable on the randomized instrument

– Plug predicted values into the equation predicting the outcome

Some Issues for IV

Where do Valid Instruments Come from?

. Valid instruments are 1) relevant and 2) exogenous

. One general way to find instruments is to look for exogenous variation – variation that is ‘as if’ randomly assigned in a randomized experiment – that affects.

– Rainfall shifts the supply curve for butter but not the demand curve; rainfall is ‘as if’ randomly assigned

– Sales tax shifts the supply curve for cigarettes but not the demand curve; sales taxes are ‘as if’ randomly assigned

Weak Instruments

. If cov(Z,X) is weak, IV no longer has such desirable asymptotic properties

. IV estimates are not unbiased, and the bias tends to be larger when instruments are weak (even with very large datasets)

. Weak instruments tend to bias the results towards the OLS estimates

. Adding more and more instruments to improve asymptotic efficiency does not solve the problem

. Recommendation always test the ‘strength’ of your instrument(s) by reporting the F-test on the instruments in the first stage regression

Summary

. A valid instrument lets us isolate a part of X that is uncorrelated with , and that part can be used to estimate the effect of a change in X on Y

. IV hinges on having valid instruments: A valid instrument isolates variation in that is ‘as if’ randomly assigned

Readings

Textbooks & Chapters

Angrist, Joshua D. and Jörn-Steffen Pischke. 2009. Mostly Harmless Econometrics: An Empiricist’s Companion. Princeton, NJ: Princeton University Press.

– One of the canonical textbooks in microeconometrics, which covers major causal inference techniques including IV, difference-in-differences, fixed effects, regression discontinuity, quantile regression, and standard error issues with major previous applications. Compared to other causal inference books, the IV part in this book is explained with more details, and in order to fully understand that part, OLS and asymptotical theory knowledge are required.

. Stephen L. Morgan and Christopher Winship. 2007. Counterfactuals and Causal Inference: Methods and Principles for Social Research. New York, NY: Cambridge University Press.

The first comprehensive survey of the counterfactual approach to causal inference from potential outcome framework, written for a social science audience with a strong emphasis on causal thinking over mathematical derivations but now somewhat outdated and the second edition is forthcoming in 2014 or 2015. One chapter is specifically devoted to IV.

. Guo, Shenyang and Mark W. Fraser. 2010. Propensity Score Analysis: Statistical Methods and Applications. Thousand Oaks, CA: Sage Publications.

– A specifically propensity-score-matching-oriented textbook, but also briefly deals with IV along with conceptually similar methods such as Heckman’s sample selection model and treatment effect model. Stata codes with related examples are provided.

. Wooldridge, Jeffrey M. 2010. Econometric Analysis of Cross Section and Panel Data. Cambridge, MA: MIT Press.

. An excellent results-oriented treatment of modern applied econometrics including IV method, a current favorite of advanced survey courses in econometrics. This book focuses more on mathematical detail and hence requires a solid working knowledge of multivariate calculus.

Methodological Articles

Angrist, Joshua D., Guido W. Imbens, and Donald B. Rubin. 1996. “Identification of Causal Effects Using Instrumental Variables.” Journal of the American Statistical Association 91(434): 444-455.

– The classic treatment of IV from a counterfactual perspective. Canonic treatment of Local Average Treatment Effect estimands.

. Martens, Edwin P., Wiebe R. Pestman, Anthonius de Boer, Svetlana V. Belitser, and Olaf H. Klungel. 2006. “Instrumental Variables: Applications and Limitations.” Epidemiology 17(3): 260-267.

– An introductory article written by epidemiologists.

. Hernán, Miguel A. and James M. Robins. 2006. “Instruments for Causal Inference: An Epidemiologist’s Dream?” Epidemiology 17(4): 360-372.

– Provides four different definitions of IV with some extentions.

. Swanson, Sonja A. and Miguel A. Hernán. 2013. “How to Report Instrumental Variables Analyses (Suggestions Welcome)” Epidemiology 24(3): 370-374.

– Provides a normative checklist for executing IV analyses.

. Bollen, Kenneth A. 2012. “Instrumental Variables in Sociology and the Social Sciences.” Annual Review of Sociology 38: 37-72.

– A recent review on IV uses from the sociology and social sciences.

Application Articles

. Angrist, Joshua D. 1990. “Lifetime Earnings and the Vietnam Era Draft Lottery: Evidence from Social Security Administrative Records.” American Economic Review 80(3): 313-336.

– Perhaps the most famous IV application.

. Acemoglu, Daron, Simon Johnson, and James A. Robinson. 2001. “The Colonial Origins of Comparative Development: An Empirical Investigation.” American Economic Review 91(5): 1369-1401.

– Another classic in IV applications using European mortality rates as an instrument.

. Kim, Daniel, Christopher F. Baum, Michael L. Ganz, S.V. Subramanian, and Ichiro Kawachi. 2011. “The Contextual Effects of Social Capital on Health: A Cross-National Instrumental Variable Analysis.” Social Science and Medicine 73: 1689-1697.

– Using corruption/population density and religious fractionalization and population density as instruments for country-level social capital.

. Fish, Jason S., Susan Ettner, Alfonso Ang, and Arleen F. Brown. 2010. “Association of Perceived Neighborhood Safety on Body Mass Index.” American Journal of Public Health 100(11): 2296-2303.

– Using household crime and neighborhood collective efficacy as instruments for neighborhood perceived safety.

. Davies, Neil, George Davey Smith, Frank Windmeijer, and Richard M. Martina. 2013. “COX-2 Selective Nonstereoidal Anti-inflammatory Drugs and Risk of Gastrointestinal Tract Complications and Myocardial Infarction: An Instrumental Variables Analysis.” Epidemiology24(3): 352-362.

– The most careful and comprehensive assessment of IV assumptions in any application.

Websites

. Applied Microeconometrics Workshop (by Guido W. Imbens and Jeffrey M. Wooldridge)

http://www.irp.wisc.edu/newsevents/workshops/appliedmicroeconometrics/schedule1.htm

. Cyrus Samii’s class website on Quant II (weeks 10-11 covering instrumental variables)

https://cyrussamii.com/?page_id=3246

Courses

. Casual Inference: Methods for Program Evaluation and Policy Research (taught by Jennifer Hill at NYU Steinhardt; offered in Fall semester)

– An application-oriented causal inference class, which deals with different causal techniques including IV from potential outcome framework, suitable for the students who do not have any exposure to causal inference concepts and methods.

. Quantitative Political Analysis II (taught by Cyrus Samii at NYU Politics; offered in Spring semester)

– A little bit techical course compared to Jennifer Hill’s, which covers some canonical textbooks and articles from a social science perspective including Mostly Harmless Econometrics (2009) andCounterfactual and Causal Inference (2007). Required some knowledge on linear algebra and econometrics, especially asymptotic theory.

. Quantitative Strategies (taught by Thomas DiPrete at Columbia Sociology; offered in Fall semester)

– Class materials are essentially the same as Samii’s one, but with more sociological research orientation.